What Key Advice Do You Need About Equity Release in 2026?

Contributors:

Expert Verified

Expert VerifiedSovereignBoss adheres to a stringent code of editorial guidelines, but some articles may feature partner references. Here is an explanation for how we make money.

Key Takeaways

- In 2026, getting clued up on the complex world of equity release with pro advice is key to making choices that fit your wallet and lifestyle.

- Start smart: Check adviser qualifications and make sure they know your situation; get the lowdown on fees; and make sure they're giving you the full picture.

- Ask about their track record, plan specifics, all costs (including consultations), and prioritise independent advice over advice tied to specific lenders for a broader view of the market.

Why is equity release advice essential when considering unlocking your property value in 2026?

If you want to join 16,691 new and returning customers that made use of equity release in Q1 of 2023,1 seek professional advice to make an informed decision based on your financial needs and avoid making hasty choices influenced by numbers alone.

We have broken down the details here.

In This Article, You Will Discover:

Our SovereignBoss team is committed to gathering accurate equity release information and presenting it in a concise and reader-friendly format.

Here are the intricacies of equity release advisers and how to obtain the best in 2026.

What Is Equity Release, and Why Is Independent Advice Crucial?

Releasing Equityfrees up cash from your home's value; independent advice is crucial to navigating options and implications effectively.

What Exactly Is Equity Release?

The process of equity release in the UK provides homeowners with a way to access funds, usually in the form of a lump sum or regular payments, while still retaining the right to live in their home.

This approach underscores the importance of equity release mortgages, highlighting how homeowners can maintain their lifestyle while accessing the financial value of their property.

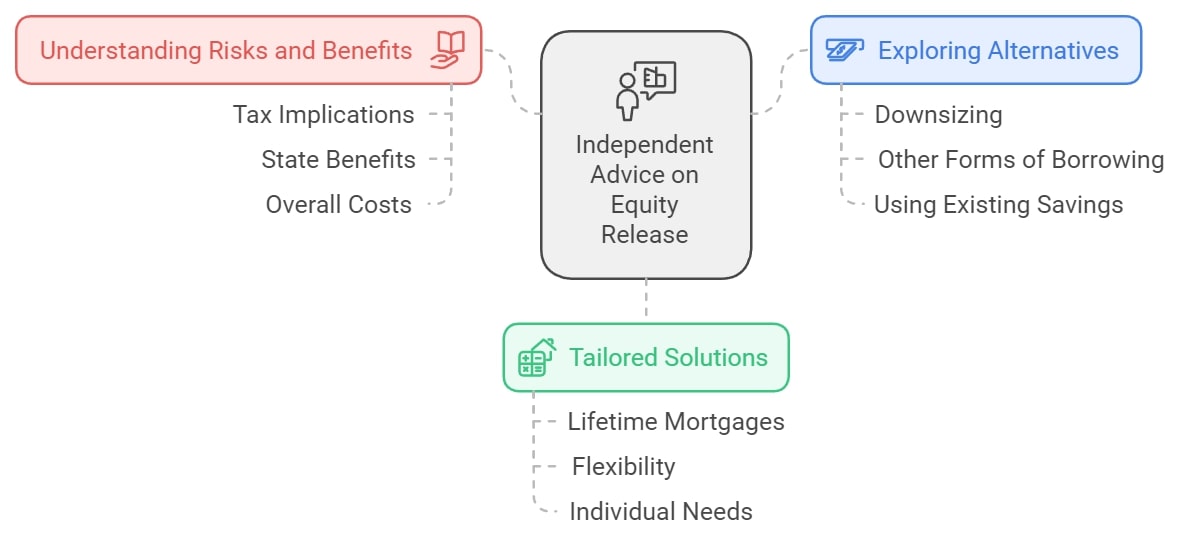

Why Should You Get Independent Advice on Equity Release? Here Are 3 Reasons

Three vital reasons to obtain advice are to understand the risks and benefits, explore all your alternative options, and find a tailored solution for your needs.

Here is a breakdown of each:

- Understanding Risks and Benefits: Equity release can seem like a straightforward way to access funds tied up in your property, but there are pitfalls and implications to consider. A professional advisor or broker can help you understand these issues, including the impact on your tax status, eligibility for state benefits, and the overall costs involved.

- Exploring Alternatives: There may be other financial options available that may suit your situation better than equity release. An advisor can help identify and explore these alternatives, such as downsizing, other forms of borrowing, or using existing savings.

- Tailored Solutions: Everyone’s circumstances are different. Fortunately, lifetime mortgages are quite flexible. A professional advisor can tailor equity release products to your individual needs, ensuring you get the right product that's best for your situation.

Is Seeking Professional Equity Release Advice Mandatory?

It is a mandatory regulatory requirement to obtain equity release advice since it is such a major financial decision.

Reputable lenders who are members of the Equity Release Council2 will insist that you seek advice from a professional adviser or broker before granting an equity release loan.

This ensures you fully understand the implications of your decision and whether it is the safest option for you.

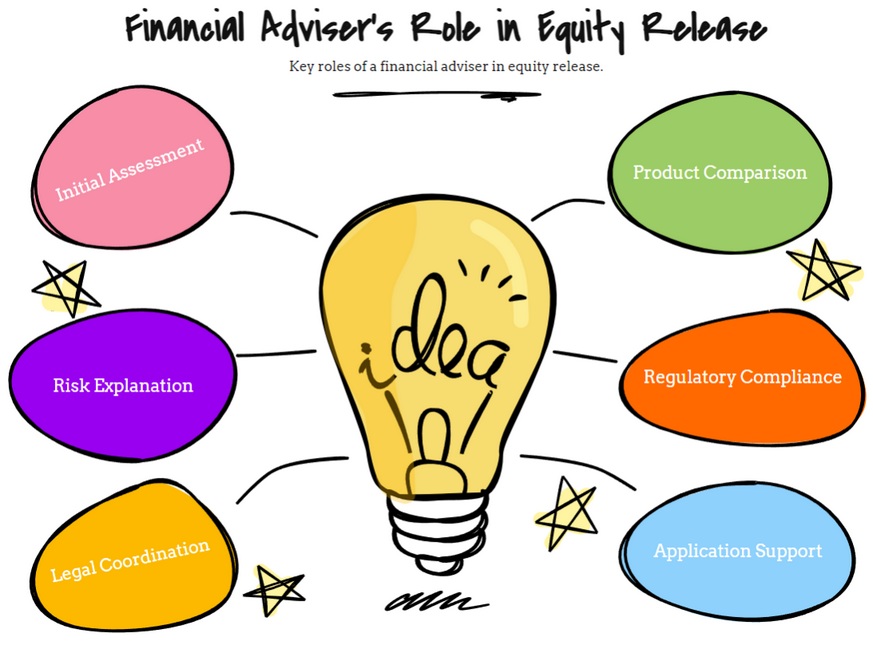

What Role Does a Financial Adviser Play in the Equity Release Process?

A financial adviser plays a pivotal role in the equity release process, beginning with assessing your financial situation to ensure equity release is a suitable option for you.

They provide a comprehensive overview of the types of plans available, help you understand the features and risks, and tailor advice to your personal circumstances.

Moreover, they'll guide you through the application process, negotiate terms on your behalf, and offer ongoing support, ensuring you make an informed decision that aligns with your long-term financial goals.

How Should You Go About Choosing the Right Equity Release Adviser?

Choose the right adviser by checking their qualifications, experience in equity release, and client testimonials for credibility and expertise.

How Do You Choose an Equity Release Adviser?

Choosing an equity release adviser involves verifying their qualifications, checking their experience, and gauging their ability to provide personalised advice.

It is important to feel comfortable discussing your financial situation with them, as you will likely be working with them for the rest of your life.

Look for advisers who are authorised and regulated in the UK by the Financial Conduct Authority3 and / or the Prudential Regulatory Authority (PRA), have positive customer reviews, and can clearly explain complex financial concepts, including being able to explain how equity release works in the UK.

Remember

Shop around to find the advisor or broker you are most comfortable with.

What Are 4 Essential Tips for Choosing an Equity Release Adviser?

Heed these 4 tips when selecting an equity release advisor:

- Independent or Tied Adviser: Consider whether the adviser is independent or tied to certain providers. An independent adviser can offer products from a fully regulated market, which could give you a wider range of options.

- Initial Consultation: Use it to gauge if you are comfortable with the adviser and if they understand your needs and objectives. Do not make a quick, in-the-moment decision.

- Understand the Fee Structure: Be clear about how and when you will be charged for the advice you receive. Ask in advance if the initial consultation is free.

- Transparency: The adviser should be upfront about all the features, benefits, risks, and costs associated with equity release. They should look at your case holistically and be transparent if equity release is not right for you.

Remember, the right adviser will help you navigate the complexities of equity release, ensuring you make the best decision based on your circumstances.

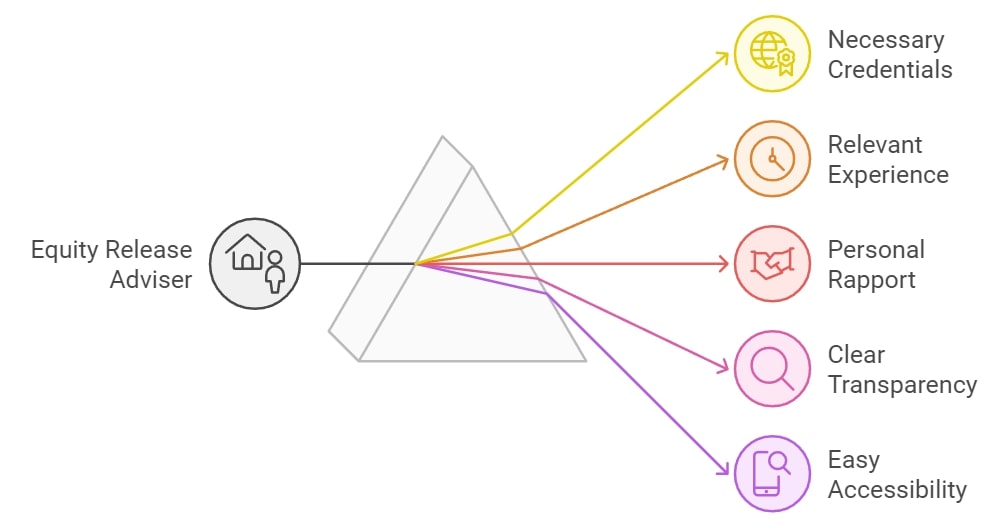

What Are Key Factors to Consider When Choosing an Equity Release Adviser?

Key factors to consider when choosing an equity release adviser must include:

- Credentials: Ensure they have the necessary qualifications and are authorised and regulated by a recognised financial authority.

- Experience: Check how long they have been practicing and their track record with equity release products.

- Personal Rapport: It is important that you feel comfortable discussing your personal and financial information with them.

- Transparency: They should be clear about their fees and how they are paid.

- Accessibility: You should be able to contact them easily when you have questions or concerns.

What Tips Can Help Select the Right Equity Release Adviser?

To select the right equity release advisers, start by creating a shortlist of potential advisers based on their qualifications, experience, and customer reviews.

Schedule initial consultations with each of them, using these meetings to evaluate their expertise and communication skills.

Very importantly

Discuss your situation and goals, and ask how they may approach your case.

Make your selection based on who best understands your needs and makes you feel the most comfortable.

You may also want to discuss your options with your heirs and ask them to provide input into the decision.

What Qualifications and Experience Should You Look for in an Equity Release Adviser?

When selecting an equity release adviser, look for someone who holds a specific qualification in equity release, such as the Certificate in Equity Release.

Experience is also crucial; an adviser with a strong track record in successfully guiding clients through equity release can offer invaluable insights and tailored advice.

Ensure they are registered with the Financial Conduct Authority (FCA) and a member of the Equity Release Council, which assures they adhere to the highest standards of advice, transparency, and protection.

How Can You Find Qualified Equity Release Advisers Near You?

You can find a qualified equity release adviser by reviewing options available on the Equity Release Council’s website.4

You can also explore these channels:

- Referrals: Ask friends, family, or colleagues for recommendations, especially those who have had a positive experience with equity release.

- Online Directories: Many professional organisations maintain directories of advisers, as mentioned above.

- Financial Institutions: Your bank or building society may offer equity release products and often have in-house advisers to assist you with the process.

- Look for Independent Financial Advisers (IFAs): They provide unbiased advice on financial matters and recommend suitable financial products available across the market.

Remember to always do your due diligence before choosing an adviser.

Which Questions Are Crucial to Ask Your Equity Release Adviser?

The types of questions you should ask an equity release adviser should be targeted to ensure they can meet your needs and provide you with the best guidance for your specific situation.

10 questions you may consider, include:

- What are your qualifications and how long have you been advising on equity release?

- Are you a member of the Equity Release Council?

- Can you explain your fee structure to me?

- Do you offer advice on all equity release products or only a selection?

- What are the implications of equity release on my entitlement to state benefits and tax situation?

- How will equity release affect the inheritance I can leave?

- Can I move home or pay off the equity release plan early?

- What are the safeguards if my provider goes out of business?

- How often will we review the equity release plan?

- What is the impact of interest roll-up and house price changes on the amount I owe over time?

What Costs Are Associated with Obtaining Professional Equity Release Advice?

Costs for professional advice can vary, including initial consultation fees, arrangement fees, and potentially a percentage of the equity released.

How Much Does Professional Equity Release Advice Cost?

The costs of professional equity release advice in the UK can vary, depending on the adviser's fee structure and the complexity of your situation.

Some advisers may charge a fixed fee, typically ranging close to the £1,500 mark.

Others may charge a fee based on a percentage of the amount you release, usually between 1.5% to 2%.5

Certain advisers offer a 'no completion, no fee service, meaning you only pay if you proceed with the equity release plan.

Always ensure the fee structure is clearly outlined before you commence.

Note that this is separate from other costs associated with setting up the equity release plan, such as application fees, valuation fees, and legal fees.

Where Can You Find Reliable and Free Equity Release Advice?

Reliable and free equity release advice can be found through various channels.

Charities and government-backed organizations often provide free guidance to help you understand your options without any financial commitment.

Additionally, many reputable equity release advisers offer a free initial consultation, which can be a valuable opportunity to gauge the adviser's expertise and approach before committing to their services.

Searching online for advisers who are registered with the Equity Release Council is a good starting point, as they are required to adhere to a strict code of conduct that ensures fairness and transparency.

Frequently Asked Questions on Equity Release Advice

What Top 10 Pieces of Advice Should You Consider for Equity Release?

What Key Considerations Are There When Seeking Equity Release Advice?

What Criteria Should You Use to Evaluate Equity Release Advice?

How Important Are Reviews When Choosing Equity Release Advice?

How Do You Verify Your Financial Adviser's Registration with the Equity Release Council?

Why Might Independent Equity Release Advice Be Preferable to Lender-Provided Advice?

What Should You Expect From a Competent Equity Release Adviser?

What Type of Information Is Provided During Equity Release Advice Sessions?

How Will an Adviser Assess the Suitability of Equity Release for My Situation?

How Can You Find Reliable and Free Equity Release Advice?

What is the Difference Between Equity Release Brokers and Financial Equity Release Advisors?

What Is the Recommended Frequency for Reviewing Equity Release Plans With Advisers?

What Steps Can You Take if Unsatisfied With Your Equity Release Adviser's Advice?

How Can Equity Release Advisers Help With Exploring Alternatives?

How Can an Adviser Help Me Understand the Impact of Equity Release on My Family and Beneficiaries?

Where Can I Get Retirement Planning Advice?

What Are the Benefits and Risks of Equity Release?

In What Ways Can Equity Release Advice Be Beneficial?

Where Can I Find Reliable Equity Release Advice?

What Constitutes the Best Equity Release Advice for Seniors?

Concluding Thoughts on Seeking Equity Release Advice

Obtaining equity release advice in the UK is crucial for those considering this significant financial step.

Equity release can provide a valuable source of funds during retirement, but it is a complex arrangement that can impact your future financial stability and the inheritance you leave to your family.

Therefore, consulting with a professional adviser, who is authorised and regulated by the FCA and / or PRA, can help navigate the maze of options and implications.

Remember, whatever your circumstances, make sure you seek out expert equity release advice to secure the best possible outcome for your financial future.